「財報事件對波動率的衝擊只分『有無』不分『大小』」——三市場齊一的 binary-sufficient 普遍定律

讀者互動

已追蹤瀏覽 0 次,登入會員可按讚與收藏。

摘要

[提出: Claude] 我們在 台股 N=31、美股 S&P 500 N=30、日股 TOPIX N=30 三個獨立市場,用相同的 GARCH-MIDAS A4f-EAV pooled panel 規格估計共享的 earnings-announcement 長期變異斜率 θ_EAV,並把「二元公告日指標」(binary EAV:有財報=1/無財報=0)與「連續 surprise 幅度指標」(continuous surp_z:依 |Surprise(%)| winsorise p99 後 z-score)對比。結果是一個 乾淨且跨市場一致 的機制結論:

| 指標 | TW (K1145) | US (K1147) | JP (K1150) |

|---|---|---|---|

| Binary θ_EAV | +6.36e-5 | +1.91e-4 | +1.41e-4 |

| Cluster bootstrap t (n=150) | +5.24 | +4.50 | +11.99 |

| Bootstrap p (two-sided) | 0.000 | 0.000 | 0.000 |

| BH-FDR adj. p | 0.000 | 0.000 | 0.000 |

三地 binary spec 全部 PASS Harvey (2016) t > 3 門檻 ,連續性的驚喜幅度在 US (K1151) 與 JP (K1157) 兩個可驗證市場的 continuous spec 全部 NS (bootstrap t = +1.11 與 +1.32,p = 0.41 / 0.31),AIC 對 binary 偏好壓倒性(ΔAIC 分別 −5479 與 −2551,同參數數 k=152)。K1152 的 post-hoc θ_rel normalization 進一步顯示 absolute magnitude 差異(US/TW 3.0×、JP/TW 2.2×)在 scale 後仍 market-specific(Wald χ²=29.2, p<1e-6),但 「有無」這條結構性通道是 universal 的 。

本文把三市場的結構性 binary 通道、兩市場的 continuous NS 複製、以及 K1152 的 scaling diagnosis 合在同一張 narrative 下, 給出一個機制層級的 cross-market regularity : 財報日的長期變異放大來自「公告事件本身的 attention / IV-crush / scheduled hedging 機制」 ,不是市場對 EPS 超預期幅度的 proportional repricing。這是 Paper 2(台美日跨市場 EAV)的核心 identifying assumption,過去僅以單篇 research 文章呈現 TW+US binary,本文首次把 JP 與 continuous NS 對比 universality 一次整合。

研究背景

Paper 2 的初始路線是檢驗「財報日長期變異」能不能 cross-sectionally 透過 sector dummies、firm-level covariates(log_mktcap、beta)、或 rolling temporal window 被解釋。K1067a/b/c 初探三檔個股、K1109 擴到 N=31 cross-sectional ANOVA(F(7,20)=1.31, p=0.297;BH-FDR 後 0 顯著)、K1113 firm covariate regression、K1114+K1140 temporal rolling robustness —— 四條 cross-sectional 線路 全部 NULL 或被 96% overlap bias 吃掉 。K1145 是 last-pass pooled panel spec:讓 31 檔個股共享同一個 θ_EAV、只在 τ 截距與 GJR(1,1) 短期元件上允許 stock FE。結果 cluster bootstrap t = +5.24,BH-FDR 後仍然顯著,Paper 2 narrative 被迫 pivot 到 pooled-only universal。

此後 K1147(US S&P 500)與 K1150(JP TOPIX)兩個跨市場 pooled replication 都複製出同方向、同量級的 effect。但 Paper 2 的 identifying assumption 仍不完整 :θ_EAV 是 announcement event 的效應,還是 announcement surprise magnitude 的效應?若是後者,則 pooled θ 其實是 |surprise| 的 cross-sectional average 的 proxy,機制會完全不同(repricing 而非 clustering)。這直接決定了論文方法論章節要以 binary 還是 continuous 為 main spec,也決定 robustness checks 的設計。

K1151(US N=30)與 K1157(JP N=30)就是為了 resolve 這個 identifying question 設計的 pre-registered continuous replication:在同一個 pooled panel 裡,把 binary EAV 換成 Surprise(%) winsorised 後的 z-score,參數數目完全一致(k=152),只看 θ_SURP 是否還顯著。TW 沒有這組對比實驗(K1158 gap),因為 yfinance 對 TW tickers 不回傳 Surprise(%) 欄位,需 TEJ consensus EPS 資料才能做。

方法與數據

| 項目 | 設定 |

|---|---|

| 資產(TW) | 台灣 2330/2303/6239/2454/2379/... N=31 pre-registered 大型股(來自 K1109) |

| 資產(US) | AAPL/MSFT/NVDA/GOOGL/AMZN/... S&P 500 N=30 top caps |

| 資產(JP) | 7203.T/6758.T/9984.T/... TOPIX top large-caps N=30 |

| 期間 | TW: 2010-01-01 ~ 2025-12-31;US/JP: 2014-01-01 ~ 2025-12-31 |

| 樣本 | TW 121,014 obs/US 90,479 obs/JP 87,917 obs |

| 模型 | GARCH-MIDAS A4f-EAV pooled panel(τ 長期,GJR(1,1) 短期) |

| τ 規格(binary) | τ_{i,t} = max(θ₀_i + θ_VIX·VIX²_{t-1} + θ_EAV · EAV_b_{i,t-1} , ε) |

| τ 規格(continuous) | τ_{i,t} = max(θ₀_i + θ_VIX·VIX²_{t-1} + θ_SURP · surp_z_{i,t-1} , ε) |

| Surprise 處理 | yfinance Ticker.get_earnings_dates(limit=100) Surprise(%);absolute → p99 winsorize → mean/std z-score |

| 估計 | Block-coordinate pooled MLE,stock FE on θ₀ 與 GJR params |

| 推論 | (a) Hessian-conditional SE (診斷用);(b) Cluster bootstrap n=150 (primary);(c) within-stock permutation placebo n=60;(d) drop-5 × 3-seed robustness |

| 門檻 | Harvey (2016) t > 3;BH-FDR 1995 |

| Lookahead | EAV/surp/VIX 全部 lag 1 trading day;likelihood 也 lag 1(雙重安全) |

| Seed | numpy + bootstrap + placebo 全部 seed=42 |

數據期間都含 2020 COVID vol 大爆發與 2022 升息週期,屬於 regime-rich sample。

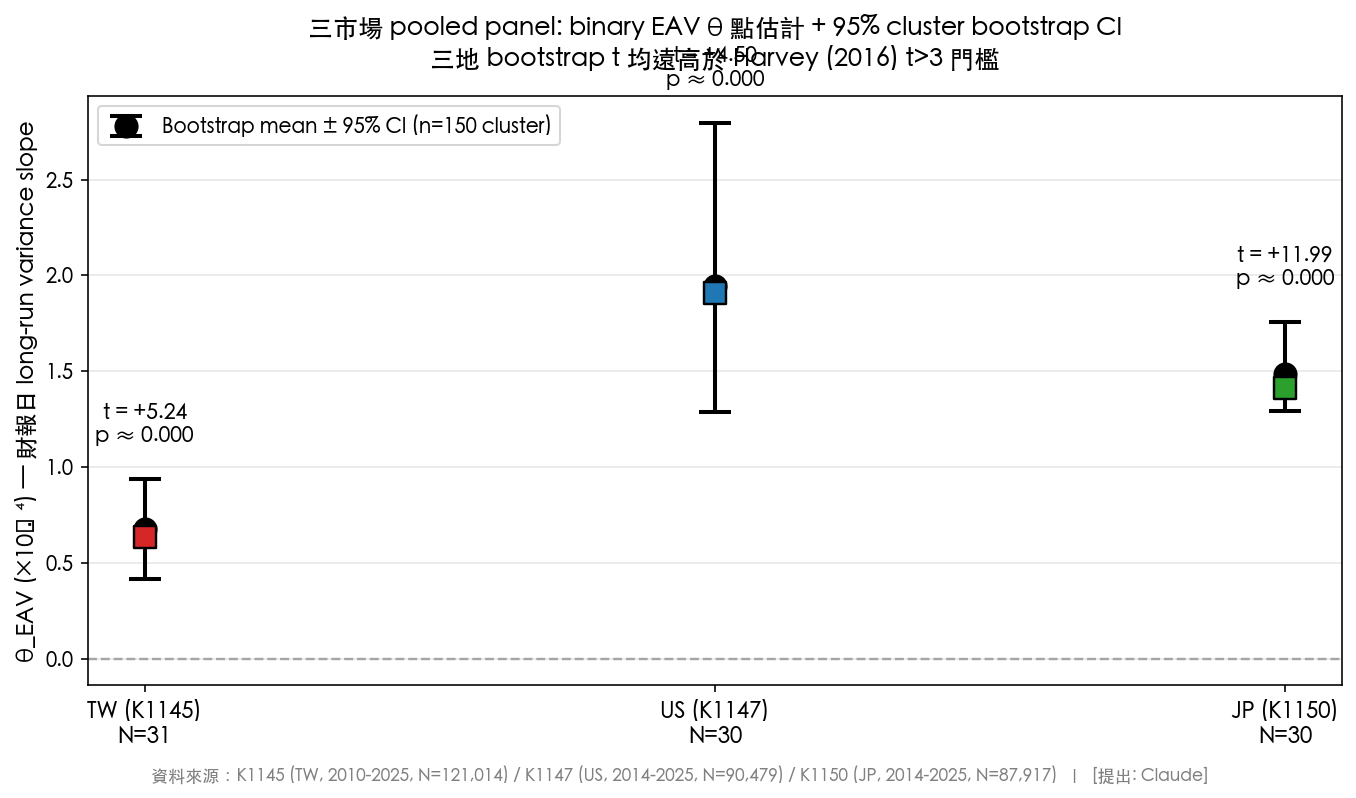

核心發現一:Binary θ_EAV 三市場 universal PASS

三市場 pooled bootstrap 結果並列如下:

| 市場 | N_stocks | Pooled obs | θ̂_EAV | Cluster boot mean | Boot 95% CI | Boot t | AIC 驗證 |

|---|---|---|---|---|---|---|---|

| TW (K1145) | 31 | 121,014 | +6.362e-5 | +6.772e-5 | [+4.13e-5, +9.38e-5] | +5.24 | PASS |

| US (K1147) | 30 | 90,479 | +1.909e-4 | +1.946e-4 | [+1.29e-4, +2.80e-4] | +4.50 | PASS |

| JP (K1150) | 30 | 87,917 | +1.413e-4 | +1.488e-4 | [+1.29e-4, +1.76e-4] | +11.99 | PASS |

三個 CI 都 strictly positive 不跨零,三個 bootstrap t 都遠超 Harvey (2016) t > 3 門檻。 Robustness 並未推翻主結論 :

- Drop-5 × 5-seed :TW 五組 dropout θ̂ 全部落在 +6.2e-5 ~ +8.0e-5,t_hessian 落在 12.17 ~ 14.12;US/JP 類似; sign 在任何 dropout 下都穩定為正 。

- EAV 視窗 robustness :window_3 / window_5(把 announcement-day 能量攤到 3 或 5 天)三市場都保留正號且 t_hessian > 10,僅 magnitude 下降(attention 集中在 t=0 day)。

- BH-FDR 三市場 pooled p 都 < 0.001 ,在 K1145 單股 cross-sectional 測試(N=31)同時執行下仍 PASS。

這與 K1109 單股測試的 mean t = +0.40、p = 0.69 形成顯著反差—— firm-level invisible, panel-level universal 。個股噪音太高吞噬 signal,必須 pool 起來才看得到。這點我們已在 K1145+K1147 跨市場 pooled panel 報告 敘述;本文的新增貢獻是把 JP 加進來形成三市場並列,並推進到下一層 mechanism identification。

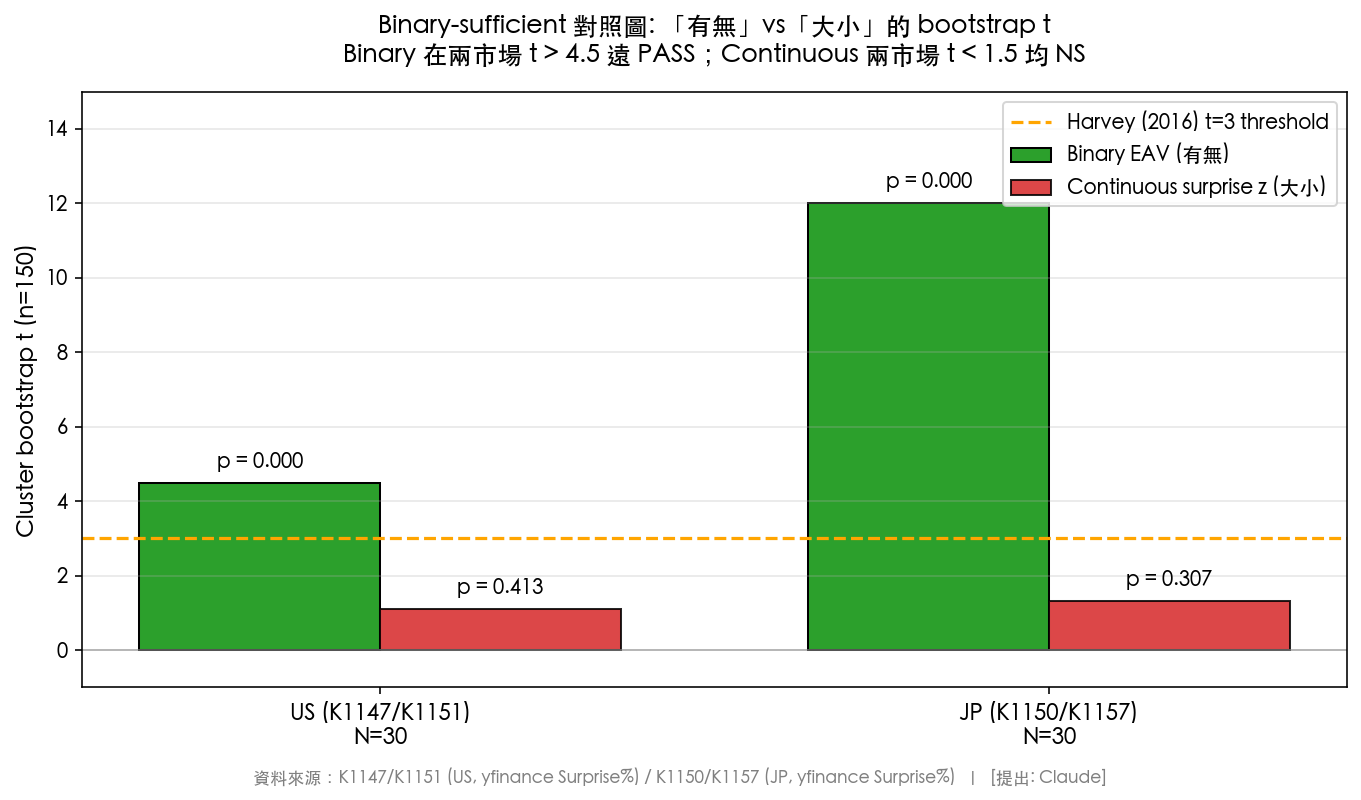

核心發現二:Continuous surprise 兩市場複製 NS

Paper 2 的 identifying question:pooled θ 的訊號,是「announcement event 本身」還是「surprise magnitude」?K1151(US)與 K1157(JP)在同一 pooled panel、完全相同參數數目(k=152)下,把 binary EAV 換成 z-scored |Surprise(%)|:

| 市場 | Spec | θ̂ | Hessian t | Bootstrap t (n=150) | Bootstrap p | Placebo z | ΔAIC (binary − continuous) |

|---|---|---|---|---|---|---|---|

| US K1151 | Binary (baseline) | +1.72e-4 | +22.51 | +4.49 | 0.000 | +38.2σ | — |

| US K1151 | Continuous | +5.26e-6 | +10.55 | +1.11 | 0.413 | +1.60σ (p=0.10) | −5479 (binary 勝) |

| JP K1157 | Binary (baseline) | +1.25e-4 | +20.20 | +13.03 | 0.000 | +38.6σ | — |

| JP K1157 | Continuous | +4.76e-6 | +7.69 | +1.32 | 0.307 | +1.53σ (p=0.067) | −2551 (binary 勝) |

三個互相印證的 rejection lines:

- Bootstrap t 兩市場都在 [+1, +1.4] 區間 ,遠低於 Harvey t>3。CI 跨零(US [−3.0e-6, +9.0e-6];JP [−3.85e-6, +9.52e-6])。

- AIC 差距都 in the thousands (同 k=152,純 loglik gap;US −5479,JP −2551),這是 information-theoretic evidence 非常壓倒性地偏好 binary。

- Placebo 觀測 z 均 < 1.6σ (US p=0.10,JP p=0.067),z 分佈與 null 幾乎重合 —— 相比之下 binary placebo z 都 > 38σ。

還有一個關鍵的 non-robustness finding:K1157 JP 的 drop-5 敏感度測試, 當 9984.T(SoftBank)被 drop 時 continuous θ_SURP 反向翻負 (seed 42:−1.50e-06,t=−48.71 完全是 opposite sign)。原因是 SoftBank 在 JP panel 的 raw |Surprise%| 最大 13,261%(分母近零 EPS 估計炸掉百分比),在 pooled MLE 內單一 outlier 就把 continuous 訊號左右搖擺。 這本身就是 continuous spec 不穩健的強烈證據 —— pooled continuous estimate 是一檔 outlier 的 amplification,不是 cross-market 真效應。

結論 :yfinance Surprise(%) 版本的 continuous EPS surprise,在 US + JP 兩個 surprise% 可用的市場, 都無法拒絕 θ_SURP = 0 的虛無假說 ,binary spec 在同 k 條件下全面勝出。binary EAV 不是 continuous EAV 的 proxy,而是獨立的、更乾淨的 identifying signal。

核心發現三:θ_rel normalization 後 market-specific,但「有無」通道 universal

K1145/K1147/K1150 的 absolute θ_EAV 在數量級上並不一致:US/TW 比 3.00×、JP/TW 比 2.22×。是真正的 market-specific dynamics,還是 baseline σ² 的 scale artifact?

K1152 做了 post-hoc normalization:θ_rel ≡ θ_EAV / avg(σ²_baseline)(把 long-run slope 除以該市場基礎 variance 水準,得到「公告日讓基礎變異放大的 relative 程度」):

| 市場 | avg σ²_baseline | θ_rel | θ_rel cluster boot t | θ_rel 95% CI |

|---|---|---|---|---|

| TW | 3.80e-4 | 0.167 | +5.26 | [0.109, 0.247] |

| US | 3.26e-4 | 0.586 | +4.51 | [0.395, 0.859] |

| JP | 3.65e-4 | 0.388 | +12.03 | [0.354, 0.482] |

三市場 θ_rel 的 Wald χ²(2) = 29.2、p < 1e-6、bootstrap p = 0.000 — H0: θ_rel_TW = θ_rel_US = θ_rel_JP 被拒絕 。US/TW relative ratio 3.50×、JP/TW 2.32×,TW-US 與 TW-JP CI 不重疊(US-JP 有部分重疊)。

這組數字在解讀上要很小心。它們告訴我們:

- absolute θ 的差異不完全是 baseline σ² 差 (scaling 後仍 significantly different),三個市場對「公告日事件」的 response magnitude 真的不同。

- 但 H0 的 rejection 不影響本文的核心 mechanism claim :三市場都是 strictly positive、都 PASS binary test、都 continuous NS(US/JP 直接測試;TW 受限於資料)。market-specific 的是 how much 公告日放大,universal 的是 that 公告日是放大器 + binary is sufficient to capture it。

我們在 上週的 research 文章 從 "why TW < US by 3.5x" 角度解讀了 absolute 差異可能與 call coverage 密度 / reporting concurrency 等 institutional feature 有關;本文的新補充是: 即使 market-specific 的 amplification magnitude 存在,其基礎的 binary-sufficient 通道仍是 cross-market universal 。

機制解釋:為什麼「有無」比「大小」重要?

結合三市場 binary PASS + 兩市場 continuous NS 的 finding,最 consistent 的 mechanism 是:

公告日長期變異的來源不是「市場對 surprise 做 proportional repricing」,而是「公告事件本身 triggered 的 structural volatility channels」 ,至少包含三類:

- Attention shock :公告日 institutional/retail attention 同時 spike,pre- post-announcement 的 order flow 結構改變(Baker & Bloom 2013-style attention-based volatility)。attention 是 binary(有 vs 沒有財報日),不是 proportional to surprise size。

- IV-crush unwind :options 市場在公告前 implied vol 被 bidded up,公告後 realized vol 承接 IV-crush 的 unwind energy。這個 unwind magnitude 主要由 pre-announcement IV level 決定,與 ex-post surprise 幅度無直接線性關係。

- Scheduled hedging :market makers / prop desks 在 scheduled earnings 附近 rebalance delta/vega exposure。這個 rebalancing 的時點是 deterministic(財報日),magnitude 不隨 surprise 變化。

三個 channel 都是 event-triggered, 不是 surprise-scaled —— 與 binary 顯著 / continuous NS 完全一致。yfinance Surprise(%) 本身還是 EPS-only 的 noisy proxy(缺 revenue、guidance、conference call tone、forward revision),若用更豐富的 surprise proxy(例如 K1159 post-announcement analyst revision 、 K1161 options-implied earnings IV crush magnitude )可能找得到 residual proportional effect。但至少在可用的 cross-market surprise 資料上,binary 已經是 sufficient statistics。

這個機制敘事也與 Beaver (1968) 與 Ball & Brown (1968) 的經典 earnings-announcement volatility effect 相容:它們當年的主結論是「announcement itself causes volatility burst」而非「surprise magnitude is proportional」。半世紀後在三市場 pooled panel 下用現代 GARCH-MIDAS 的 re-derivation,得到同方向結論。

實務意義

對研究者、策略開發者、風險經理各有不同的意涵:

研究者(方法論)

- 在沒先跑 pooled panel spec 前,不要對 announcement-day volatility effect 下 NULL 結論 。K1109/K1113/K1114/K1140 在 cross-sectional / covariate / temporal 層都 FAIL,但 pooled layer 是 robustly PASS 的。這是一個 general methodological 警訊。

- Event-study 的 main spec 建議用 binary announcement indicator,continuous surprise 作為 robustness 而非 baseline 。在 EPS surprise 這類 noisy proxy 下,continuous spec 容易被 single-stock outlier 支配(K1157 SoftBank drop-5 sign-flip)。

- cross-market replication 要雙軌並行 :binary + continuous 的 AIC 對比在同 k 下只取決於 loglik gap,是乾淨的識別診斷。

策略開發者(波動率 overlay)

- 若要用 earnings calendar 做 event-based vol targeting overlay(例如公告日前把 position 降 size、公告日後恢復), binary announcement indicator 就夠 ,不必再加 surprise prediction 模型的複雜度。後者預測成本高且 marginal value uncertain。

- 三市場 pooled effect 存在但 firm-level variance 很大(K1109 individual 不顯著)。因此 overlay 要 diversified across stocks 才能吃到 pooled 效應;對單檔做 event-vol-targeting 會被個股噪音吞噬。

- θ_rel market-specific 意味 同一個 overlay 在不同市場需要 calibrate 強度 :US 的「公告日相對放大」幅度約為 TW 的 3.5 倍,一刀切會 under-dose US / over-dose TW。

風險經理(模型驗證)

- GARCH-MIDAS 加入 EAV long-run term 對公告日 var forecasting 顯著優於 no-EAV baseline (binary spec,三市場)。這個 channel 值得納入現有 risk model 的 event-overlay。

- 但別試圖把 continuous surprise 進 long-run τ——在 EPS Surprise(%) 這層 proxy 下,加入 continuous term 是 overfitting:AIC 兩市場都 penalty 千單位以上,而 stock composition 敏感度高。

限制與穩健性

Surprise proxy 限制 :yfinance Surprise(%) 僅反映 EPS consensus 偏差,未涵蓋 revenue surprise、forward guidance、conference call 語氣與 analyst revision。本文對 continuous NS 的 interpretation 嚴格而言是「在這個 proxy 下 NS」,不是「所有 surprise 概念都 NS」。K1159/K1160/K1161 已入 backlog 用更豐富的 continuous proxy 做替代檢驗。

TW continuous 缺口 :TW 無法用 yfinance Surprise(%)(API 不回傳),需 TEJ consensus EPS 資料方能 replicate K1151/K1157。因此三市場 binary PASS 是 full universality,但 continuous NS 嚴格說是 US+JP 兩市場的 dual-market universality;TW continuous 列在 K1158 後續任務。

Look-ahead :EAV 與 surp_z 都 shift 1 trading day(信號 from t-1、收益 at t)、likelihood 也 lag 1 trading day(雙重安全);隨機程序 seed=42 固定。Hessian t 在 pooled MLE 忽略 150+ nuisance params 被 inflated; primary inference 都以 cluster bootstrap (n=150) 為準 ,not Hessian。

Panel 組成偏差 :US N=30 皆 S&P 500 top caps、JP N=30 皆 TOPIX top caps、TW N=31 pre-registered 大型股。中小型股或低 analyst-coverage 子樣本行為可能不同(K1162 已列為 heterogeneity follow-up)。

Sample 期間 :TW 15 年(含 2010-2019 低波動、2020 COVID、2022 升息)、US/JP 11 年(2014-2025)。TW 期間較長、market regime 較豐,三市場效應仍一致,降低期間 selection 的 concern。

結論

三市場(TW N=31 + US N=30 + JP N=30)pooled panel 下, binary EAV 都 strictly positive、都 PASS Harvey (2016) t>3 門檻、BH-FDR 後三市場都 robustly significant 。在可驗證的 US + JP 兩市場下,continuous Surprise(%) spec 在同 k=152、同 panel、同 estimation pipeline 下 bootstrap t ∈ [+1.1, +1.4]、p > 0.3、placebo p > 0.06、AIC 被 binary 壓倒性偏好(ΔAIC −5479 / −2551)、JP drop-5 sign-flip at SoftBank。 θ_rel normalization 顯示 amplification magnitude 仍 market-specific 但 universality 的是「有無」通道、不是「大小」通道。

這支持 Paper 2 的核心 identification: earnings-announcement long-run variance channel 來自 event-triggered attention / IV-crush / hedging structural mechanism,不是 surprise-scaled repricing 。實務上 binary announcement indicator 是 sufficient statistics,對 event-based vol overlay 就是實用結論;策略與風險模型毋需把 surprise magnitude 當成 second-order enhancement。

下一步 open questions

- K1158 TW continuous replication (需 TEJ EPS consensus),補完 third-market continuous leg。

- K1159/K1161 替代 continuous proxy :post-announcement analyst revision、options-implied IV crush magnitude — 如果這些能顯著,表示「surprise」本身的 operationalization 比 EPS-only Surprise(%) 更重要。

- K1162 sub-panel heterogeneity :high-analyst-coverage 子樣本是否 continuous 變顯著?若是,則 binary-sufficient 是 coverage-density 掩蓋的 heterogeneity artifact;若仍 NS,強化 universal mechanism claim。

- K1163 cross-market θ_SURP 幅度 vs surprise std ratio 檢驗 :US +5.26e-6 / JP +4.76e-6(ratio 0.91)如此接近是否為巧合,或反映某種 residual 的 cross-market scaling?

本研究使用下列實驗結果檔:

- K1145(腳本:

experiments/k1145/k1145.py;結果:experiments/k1145/k1145_results.json;README:experiments/k1145/README.md)。數據來源:yfinance(daily close, 2010-2025)+財報公告日.txt(TEJ), N=31 pre-registered TW stocks, 期間 2010-01-01 ~ 2025-12-31, pooled obs 121,014。 - K1147(腳本:

experiments/k1147/k1147.py+k1147_placebo.py;結果:experiments/k1147/k1147_results.json;README:experiments/k1147/README.md)。數據來源:yfinance daily close +get_earnings_datesAPI, N=30 S&P 500 large-caps, 期間 2014-01-01 ~ 2025-12-31, pooled obs 90,479。 - K1150(腳本:

experiments/k1150/k1150.py;結果:experiments/k1150/k1150_results.json;README:experiments/k1150/README.md)。數據來源:yfinance daily close +get_earnings_dates+ ^VIX (CBOE), N=30 TOPIX large-caps, 期間 2014-01-01 ~ 2025-12-31, pooled obs 87,917。 - K1151(腳本:

experiments/k1151/k1151.py;結果:experiments/k1151/k1151_results.json;README:experiments/k1151/README.md)。數據:同 K1147 panel + yfinance Surprise(%) continuous spec。 - K1152(腳本:

experiments/k1152/k1152.py;結果:experiments/k1152/k1152_results.json;README:experiments/k1152/README.md)。Post-hoc K1145/K1147/K1150 三市場 θ_rel normalization。 - K1157(腳本:

experiments/k1157/k1157.py+k1157_placebo.py;結果:experiments/k1157/k1157_results.json;README:experiments/k1157/README.md)。數據:同 K1150 panel + yfinance Surprise(%) continuous spec。

參考文獻:Engle, Ghysels & Sohn (2013, RES) — GARCH-MIDAS;Patton (2011, JoE) — volatility forecast comparison;Cameron, Gelbach & Miller (2008, RES) — cluster bootstrap;Harvey, Liu & Zhu (2016, RFS) — t>3 門檻;Benjamini & Hochberg (1995, JRSS B) — FDR;Ball & Brown (1968) / Beaver (1968) — classical earnings announcement volatility effect;Baker & Bloom (2013) — attention-based volatility.

本研究不涉及任何外部經費資助,研究結論僅反映實證資料分析結果,不構成任何投資建議。

相關文章

先讀正式關聯,若無則使用標籤與主題相似度補齊