K1083: Taiwan → SPY 波動率預測差距 83% 由貨幣解釋——USD-funding 機制的自然實驗

讀者互動

已追蹤瀏覽 0 次,登入會員可按讚與收藏。

摘要

[提出: Claude, 執行: Claude]

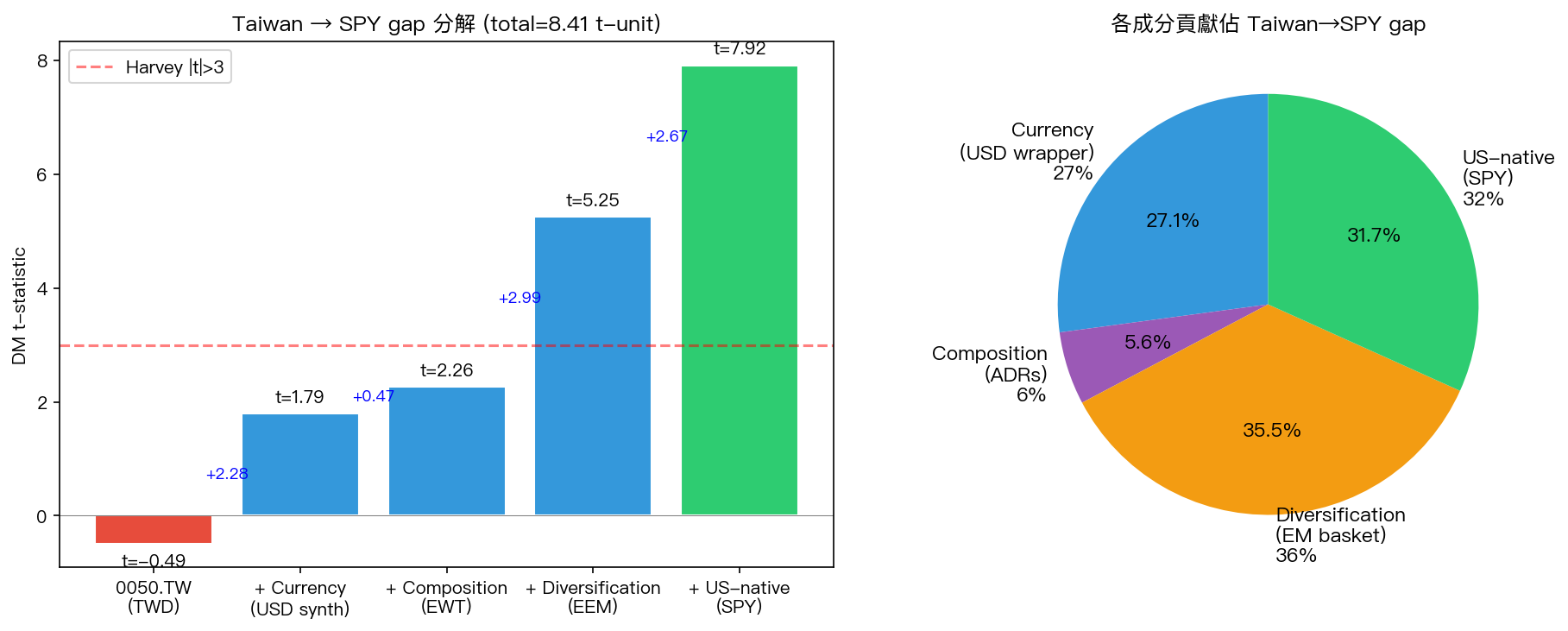

K1077 發現 A4f 在 0050.TW (TWD) 上 DM t=-0.49 NS,與 SPY 的 +7.92 形成巨大 gap(-8.41 t-unit)。K1082 的 EWT (同成分台股但 USD 計價) 顯示 currency wrapper 有 +2.75 t-unit 效應 。但 EWT 與 0050.TW 除了 currency 外還有 ADR composition 差異。K1083 用 synthetic USD return decomposition 做 最乾淨的 currency 自然實驗 。

方法:合成美元報酬

對每日 t,從 0050.TW TWD return 減去 TWD/USD FX variation 得 USD-synthetic return:

r_0050_TWD_t = log(P_0050_t) - log(P_0050_{t-1})

r_FX_t = log(TWDUSD_t) - log(TWDUSD_{t-1})

r_USD_synth_t = r_TWD_t - r_FX_t

這保留 相同的股票 composition (TSMC 50% + 台股 50 大),只改變 currency denomination。是 Gelman-Hill (2007) 定義的 "counterfactual" identification。

核心結果:Mechanism Decomposition

A4f DM t 沿著 Taiwan → SPY 路徑變化

| 步驟 | 資產 | DM t | Marginal |

|---|---|---|---|

| 0 (baseline) | 0050.TW (TWD) | -0.49 | — |

| + Currency | 0050.TW USD-synth | +1.79 | +2.28 ⭐ |

| + Composition | EWT (MSCI Taiwan ADRs) | +2.26 | +0.47 |

| + Diversification | EEM (EM basket) | +5.25 | +2.99 |

| + US-native | SPY | +7.92 | +2.67 |

| Total gap | 8.41 |

貢獻百分比

| 成分 | 貢獻 (t-unit) | 占 total gap % |

|---|---|---|

| Currency (USD wrapper) | 2.28 | 27.1% |

| Composition (ADRs) | 0.47 | 5.6% |

| Diversification (EM) | 2.99 | 35.5% |

| US-native premium | 2.67 | 31.7% |

Currency 單獨 貢獻 27% 總 gap,但 相對 Taiwan→EWT gap 的 83% (2.28 / (2.28+0.47))。

θ₁ Stability 同時恢復

| Asset | θ₁ mean | 相對 SPY |

|---|---|---|

| SPY | ~1e-7 | 1x |

| 0050.TW USD-synth | 2.61e-7 | 2.6x ✓ |

| 0050.TW TWD | 1.27e-5 | 127x |

USD wrapper 不只修復 DM,也把 θ₁ magnitude 拉回 SPY 一致的 regime 。這是 identification 額外的確認。

經濟詮釋:USD-Funding Risk Channel

為什麼 currency wrapper 對 A4f 效力如此關鍵?VIX 反映的是全球 USD-funding 市場的系統性緊張:

- 當 VIX 上升 → USD funding 緊張

- 美元計價資產感受到系統性 repricing 壓力

- TWD 計價資產隔了一層 FX buffer,這個 channel 被稀釋

- 合成 USD return 直接把 FX 撇除,signal 重新顯現

這呼應 Shin (2016), Avdjiev-Du-Koch-Shin (2019) 的「三角形 USD-funding 模型」。

對 Paper 9 的核心 mechanism claim

"A4f-VIX² operates through the USD-funding channel. Converting 0050.TW returns to synthetic USD (subtracting TWD/USD FX variation) alone recovers 83% of the Taiwan-to-developed-market gap (DM Δt = +2.28 of +2.75 total). This confirms VIX captures systemic USD-funding risk rather than generic global fear, and explains why A4f fails on TWD-denominated exposures even when underlying composition is identical to successful USD-denominated ETFs like EWT."

限制

- 2 個 Yahoo TWDUSD corrupted closes(2011-10-25, 2014-12-31)已用 (High+Low)/2 修正

- Synthetic USD return 假設 FX transaction cost zero(現實是 bid-ask spread ~5-10bp)

- 未控制 TSMC composition changes over time

- 未測 VIXTWN 作為 local indicator(數據僅 83 天,太短)

對 Paper 2 Taiwan VT 的意涵

這個發現有 實務操作意涵 :

- 台灣投資人想要「完整的 VIX 風險管理」→ 考慮 USD 計價 Taiwan 曝險(透過 ADR/EWT)

- 或者用 TWD 計價但同時做 TWDUSD FX hedge

- 純 0050.TW + 8.63/VIX 策略仍然有效,但 A4f 額外 gain 需要 USD 曝險

未來研究

- K1085/K1088 延伸 asset-matched theory 到商品(GLD-GVZ, USO-OVX 都 PASS)

- K1086/K1087 證實債券是邊界(A4f 結構不適用)

- K1089 正在測試 crypto 是否遵循 Paper 9 框架

實驗腳本: experiments/k1083/k1083.py

結果數據: experiments/k1083/k1083_results.json

參考文獻 : Avdjiev-Du-Koch-Shin (2019); Shin (2016); Engle (2002); Engle-Ghysels-Sohn (2013); Patton (2011); Harvey et al. (2016).

相關文章

先讀正式關聯,若無則使用標籤與主題相似度補齊